Financial Tools

How to Achieve Financial Freedom with SIP Investing

Build a long-term SIP plan for financial freedom with step-up contributions, inflation-adjusted views, and year-wise growth—all calculated locally in your browser.

By UseBoldTools Team 9 min readPublished July 2, 2026

Introduction

Financial freedom is not a lottery ticket—it is usually a decades-long combination of spending discipline, manageable debt, emergency reserves, and consistent market participation. For many salaried households in India, the most practical entry point into market-linked investing is a Systematic Investment Plan (SIP): a fixed mutual fund contribution every month that turns wealth building into a recurring habit instead of a one-time gamble on market timing.

This guide explains how to achieve financial freedom with SIP investing using the free SIP Calculator on UseBoldTools as your planning workspace. You will model long tenures, enable step-up SIP as income grows, read inflation-adjusted outcomes, and use the year-wise breakdown to see when compounding starts doing the heavy lifting—all in your browser without an account.

New to return estimates? Start with how to calculate SIP returns before investing. If you already know your freedom number, jump to how much you should invest every month to reach your goal. More guides are on the UseBoldTools blog.

What financial freedom means in SIP terms

Financial freedom is personal. For some it means retiring at 50; for others it means working on passion projects without paycheck stress, funding a child’s education without loans, or building a rental-income buffer. In SIP terms, freedom is the point where invested assets—plus other income sources—can sustain your chosen lifestyle.

SIP does not deliver that outcome next quarter. It supplies the engine: regular contributions, rupee-cost averaging through market ups and downs, and compounding over years. The calculator helps translate “I want freedom someday” into “here is what ₹12,000 monthly might become in 20 years at 12%” or “here is the SIP I need for ₹2 crore.”

Freedom planning also requires honesty about expenses. A corpus that looks adequate on a spreadsheet may fail after inflation, healthcare costs, or lifestyle upgrades. That is why this tool pairs nominal maturity with optional inflation adjustment and planning notes when assumptions look aggressive.

What the SIP Calculator does for freedom planning

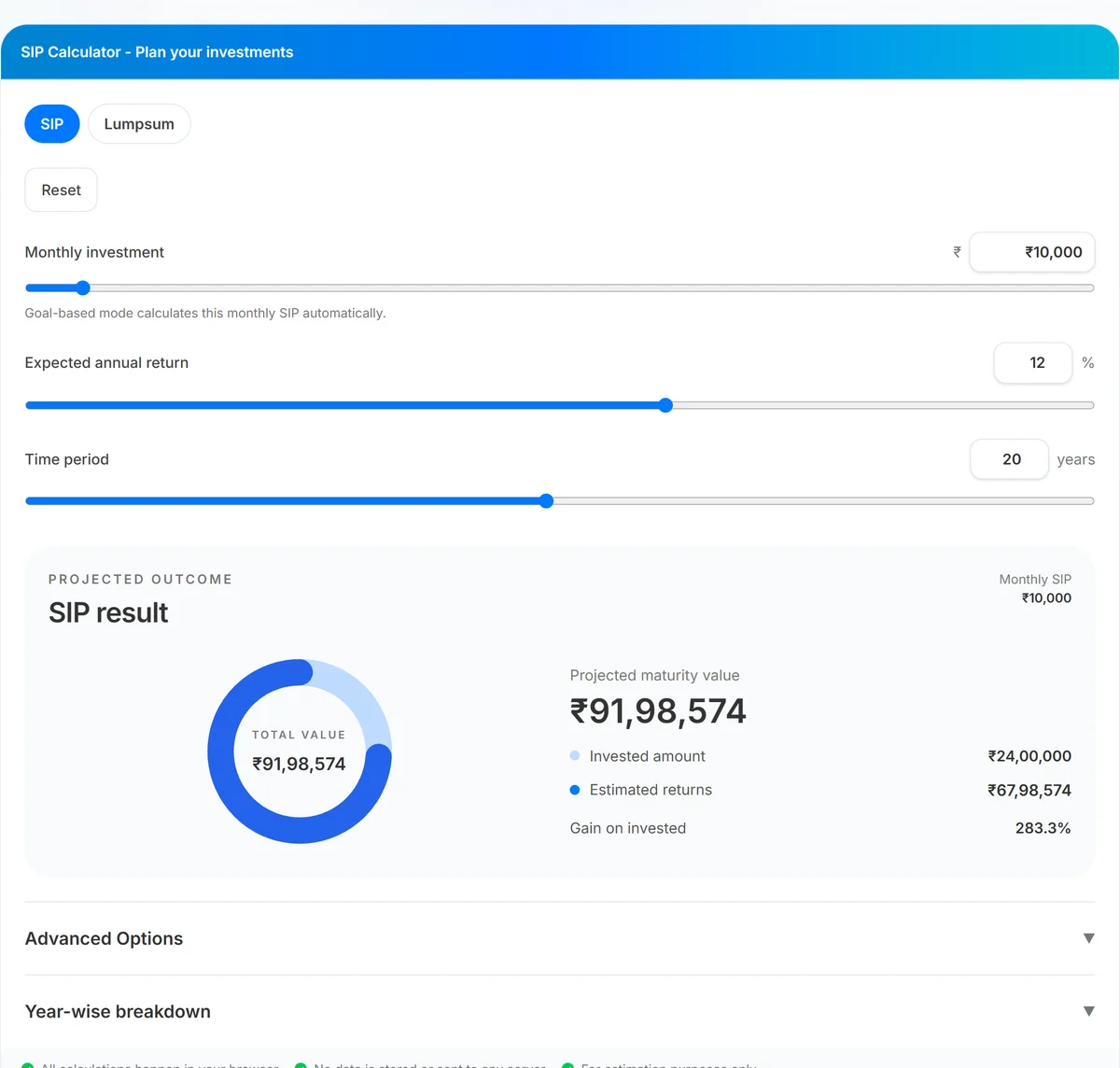

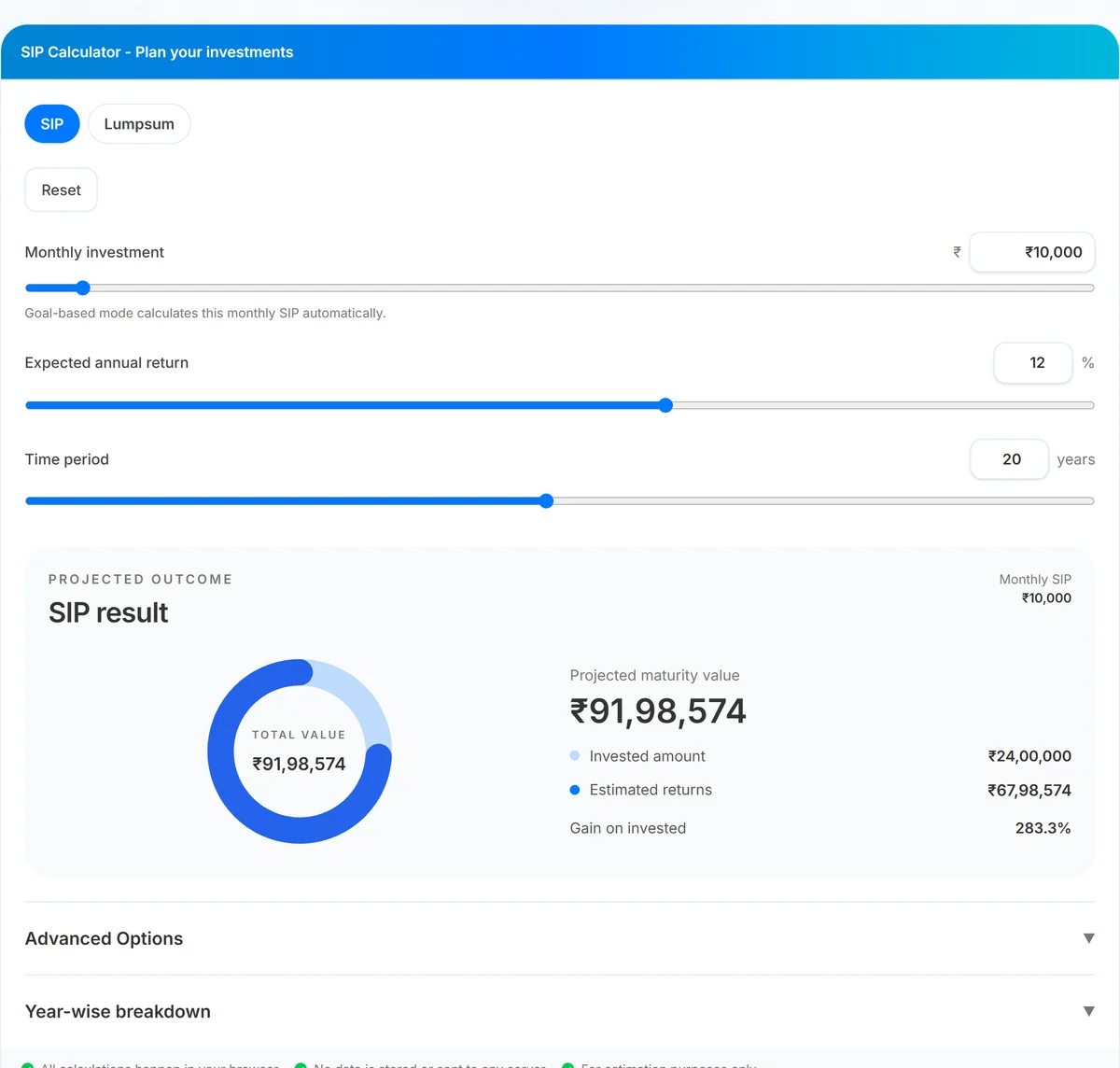

UseBoldTools SIP Calculator is built for multi-year scenarios—not quick napkin math. SIP mode projects recurring contributions; Lumpsum mode models deploying a windfall today. Advanced Options add step-up SIP (annual % or fixed increase), goal-based reverse planning (monthly SIP for a target corpus), and inflation-adjusted “real value today.”

The projected outcome panel shows total value, invested capital, estimated returns, and a donut chart so you see how much of your freedom fund comes from your savings rate versus growth. The year-wise breakdown table reveals acceleration: early years are dominated by contributions; later years often show returns outpacing new money.

Planning notes warn when targets imply unrealistic monthly SIP amounts, when inflation meets or exceeds return assumptions, or when lumpsum comparisons use mismatched scales. Those guardrails keep long-term dreams tethered to cash-flow reality.

When SIP fits a financial freedom roadmap

- Steady salary income. SIP aligns with monthly paychecks better than waiting to invest “when the market dips.”

- Long horizon goals. Freedom targets fifteen or more years away benefit most from compounding—duration is a lever you control.

- First-time equity exposure. Smaller monthly entries reduce the psychological barrier of investing a large lumpsum at the wrong moment.

- Rising income careers. Step-up SIP models annual increases so your freedom plan grows with promotions.

- Parallel debt management. Households with home loans can model EMIs in the EMI Calculator and route remaining surplus to SIP once high-interest debt is cleared.

SIP is less ideal when you need the money within two to three years—short horizons belong in safer instruments. Freedom planning is inherently long dated; match fund categories and return assumptions to that reality.

Step-by-step: model a freedom-oriented SIP plan

Open SIP Calculator. Start in SIP mode with a monthly amount you can sustain through a market downturn—not just a bull market bonus month.

- Define a freedom horizon. Set tenure in years to your target age or milestone (e.g., 25 years to age 55).

- Pick conservative and base return rates. Run 10% and 12% scenarios for equity-heavy plans; use lower rates for hybrid or debt-oriented allocations.

- Enable step-up SIP. Open Advanced Options → Step-up SIP → choose Annual % (e.g., 10% yearly increase) or fixed rupee step-up aligned with expected raises.

- Turn on inflation adjustment. Set an inflation rate (6% is a common planning default in India) and read “real value today” beside nominal maturity.

- Use goal-based mode when you know the corpus. Enable Goal-based SIP, set a target (₹1 crore, ₹2 crore, etc.), and read the required monthly SIP in the results panel.

- Study the year-wise breakdown. Identify when total value crosses meaningful milestones—first ₹25 lakh, ₹50 lakh, ₹1 crore under your assumptions.

- Compare Lumpsum for windfalls. Bonuses or inheritance may jump-start freedom; switch modes to see if a partial lumpsum plus SIP beats SIP alone.

Step-up SIP and inflation: the freedom multipliers

A flat ₹10,000 SIP from age 28 to 58 is a strong start—but if your income doubles and your SIP stays flat, your savings rate as a percentage of pay actually falls. Step-up SIP fixes that drift. A 10% annual increase on a ₹10,000 start means you contribute more each year without a single painful jump.

Inflation is the silent opponent of freedom. A ₹3 crore nominal corpus three decades from now may fund a middle-class lifestyle—or fall short if education, housing, and medical costs outpace your assumptions. The calculator’s inflation-adjusted view converts future value into approximate today’s rupees so you plan for purchasing power, not bragging rights.

When inflation rate meets or exceeds your expected return, planning notes flag that real wealth may grow slowly even when the headline number rises. That is a signal to increase contributions, extend tenure, or revisit asset allocation—not to abandon the plan.

Benefits of SIP for long-term financial freedom

- Habit over timing. Automatic monthly investing removes the need to predict market bottoms.

- Rupee-cost averaging. You buy more units when prices are lower and fewer when higher—smoothing entry across cycles.

- Compounding tailwinds. Long tenures let returns earn returns; the year-wise table makes that visible.

- Scalable contributions. Step-up SIP ties freedom planning to career growth.

- Transparent local math. Browser-based estimates let you iterate privately before talking to family or advisers.

- Goal reverse engineering. Freedom number known? Goal mode outputs the monthly SIP required instead of vague “save more” advice.

Privacy and security

Freedom plans involve salary figures, net worth targets, and timelines you may not want stored on a server. UseBoldTools SIP Calculator runs entirely in your browser. Inputs are not transmitted for calculation or logged in a personal account—there is no account to begin with.

The tool footer confirms local processing and estimation-only output. Use private browsing or close the tab on shared computers. This calculator does not execute trades, link to demat accounts, or store portfolio data.

Estimates are educational. Mutual fund returns vary; regulatory and tax rules change. Pair calculator output with professional advice for asset allocation, insurance, and estate planning.

Common mistakes on the path to financial freedom

- Chasing returns instead of savings rate. A higher monthly SIP often beats hunting for an extra 1% return assumption on paper.

- Stopping SIP during downturns. Volatility is expected; pausing destroys rupee-cost averaging benefits.

- Ignoring EMIs and high-interest debt. Freedom delayed by 18% credit-card debt is real—model loans with the EMI Calculator first.

- Flat SIP forever despite rising income. Lifestyle inflation consumes raises unless step-up SIP captures part of each hike.

- Using nominal corpus for retirement spending. Always cross-check inflation-adjusted value for 15+ year goals.

- Single-scenario planning. Run conservative and base cases; freedom plans should survive bad years, not only average ones.

For forward return math fundamentals, see how to calculate SIP returns before investing. For monthly amount targeting, see how much you should invest every month to reach your goal.

Best practices for freedom-focused SIP investors

- Automate the SIP mandate on payday so the money moves before discretionary spending.

- Increase contributions after every raise—even 50% of the hike redirected to SIP compounds meaningfully over decades.

- Keep six to twelve months of expenses in liquid savings before maximizing equity SIP aggression.

- Review fund performance annually with ${CAGR} thinking—replace chronic underperformers, do not churn quarterly.

- Separate goal buckets mentally: freedom corpus versus near-term goals may need different fund categories and tenures.

- Re-run SIP Calculator yearly with updated income, inflation assumptions, and freedom target.

Conclusion

Financial freedom with SIP investing is less about a perfect fund pick and more about decades of consistent contributions, rising savings rates, and realistic assumptions about returns and inflation. UseBoldTools SIP Calculator lets you model that journey with step-up SIP, goal-based planning, charts, and year-wise detail—locally in your browser.

Start today: open SIP Calculator, set your freedom horizon, enable step-up and inflation views, and read the projected outcome before you increase—or begin—your monthly mandate. More guides await on the UseBoldTools blog.

Frequently asked questions

Can SIP investing lead to financial freedom?

SIP is a disciplined savings and investment habit, not a shortcut. Financial freedom usually means investments and passive income cover living expenses. SIP helps build that corpus over long tenures when combined with realistic return assumptions, step-up contributions, and controlled debt.

How much should I invest monthly for financial independence?

Start with a sustainable percentage of take-home pay—often 15–30% for aggressive planners, less for households with heavy EMIs. Use goal-based mode on the SIP Calculator to work backward from a target corpus and compare the required monthly SIP against your budget.

What is step-up SIP and why does it matter?

Step-up SIP increases your monthly contribution each year by a percentage or fixed rupee amount. It mirrors salary growth so your investment rate rises with income instead of staying frozen at your first-job contribution level.

How does inflation affect a financial freedom plan?

Future corpus values look larger in nominal rupees, but inflation erodes purchasing power. Enable inflation adjustment on the calculator to see real value in today’s money and avoid retiring on a number that feels big but buys less.

Should I pay off loans before starting a SIP?

High-interest debt often deserves priority. Model your EMI with the EMI Calculator, keep an emergency fund, then route surplus to SIP. There is no single rule—compare interest saved versus long-term investment growth under conservative assumptions.

Related guides

How to Calculate SIP Returns Before Investing

Estimate SIP maturity, compare lumpsum outcomes, and read year-wise growth before you invest. UseBoldTools runs all calculations locally in your browser.

How Much Should You Invest Every Month to Reach Your Goal?

Find the monthly SIP required for your target corpus with goal-based planning, step-up SIP, and inflation context—calculated locally in your browser.

Related tools

Ready to try SIP Calculator?

Use our free SIP Calculator tool in your browser — no account required for most workflows.

Open SIP Calculator