Financial Tools

Common Home Loan Mistakes First-Time Buyers Make

Avoid common home loan mistakes as a first-time buyer: model EMI and total interest with UseBoldTools, compare tenure, plan prepayments, and balance investing with SIP.

By UseBoldTools Team 7 min readPublished July 2, 2026

Introduction

Buying your first home is exciting—and easy to get wrong on the numbers. Sales conversations focus on property price and monthly EMI, while total interest, insurance add-ons, tenure trade-offs, and future prepayment capacity stay in the background. Before you sign a sanction letter, model the loan with the free EMI Calculator on UseBoldTools so you see EMI, total repayment, and interest alongside your budget.

This guide covers common home loan mistakes first-time buyers make and how to avoid them using the UseBoldTools calculator workflow. You will learn what to enter for a typical home loan, which outputs deserve the most attention, and how mistakes compound over a 15- or 20-year tenure. Complement this with EMI vs total interest explained for cost literacy and how prepayments reduce loan interest when you plan bonuses toward principal.

Explore more guides on the UseBoldTools blog.

First-time buyers often juggle property visits, legal due diligence, and loan paperwork simultaneously. It is easy to accept the first sanction letter that clears EMI comfort without stress-testing total interest or future rate scenarios. Blocking thirty minutes to model two or three loan structures in the calculator before site visits can narrow your property budget to what you can truly afford over decades—not just this month.

What the EMI Calculator shows home buyers

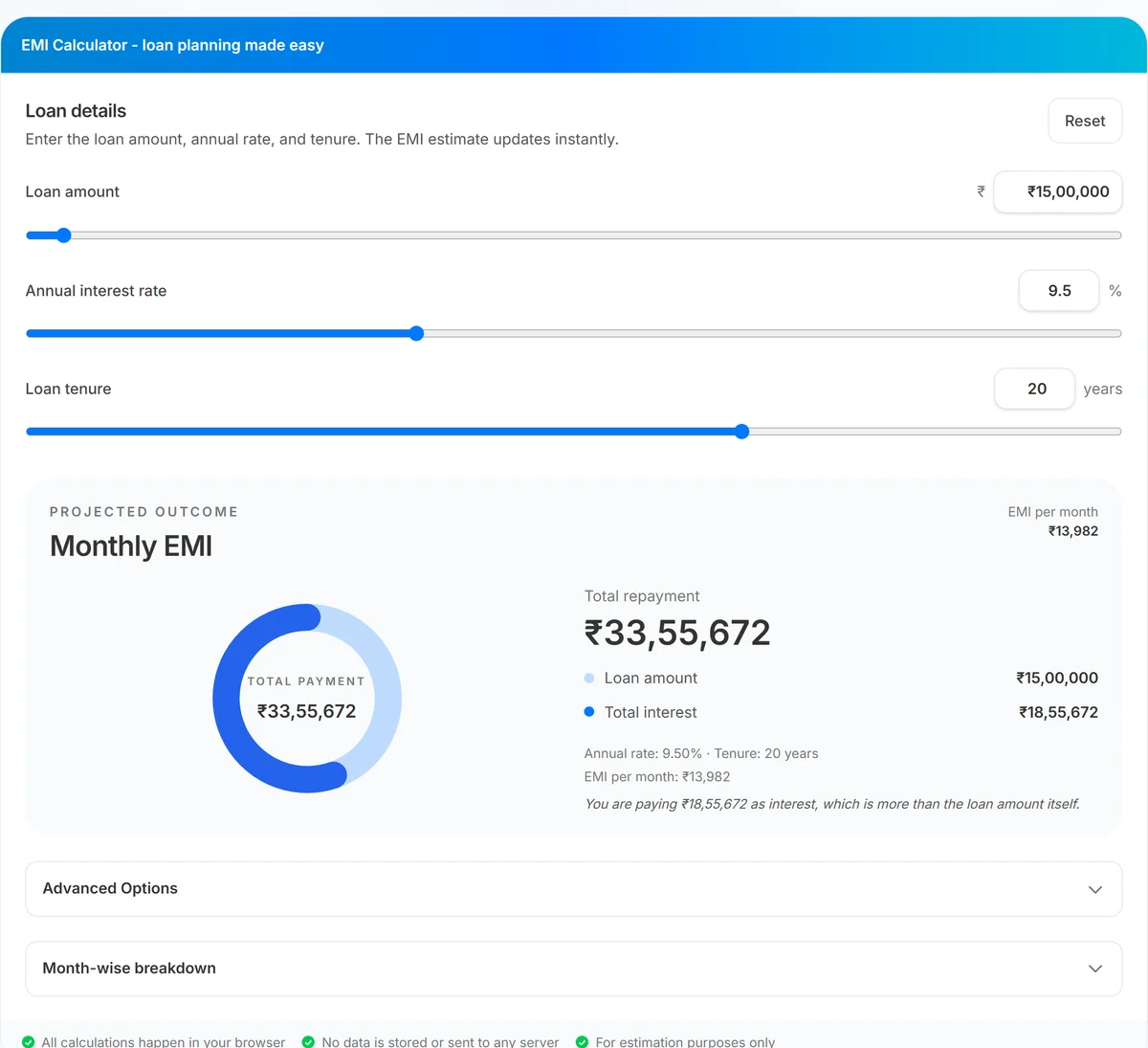

UseBoldTools EMI Calculator accepts loan amounts from ₹1 lakh to ₹5 crore, annual rates from 1% to 25%, and tenures from 1 to 30 years—enough range for most residential mortgages. Enter principal after your down payment, not the full property price. Results show monthly EMI, total payment, total interest, and a principal-vs-interest donut chart.

Advanced Options simulate prepayment—critical for home loans where partial payments can save lakhs. Month-wise breakdown exposes how slowly principal drops in early years, which explains why buyers who only look at EMI underestimate long-term cost.

Calculations are browser-local with no account. Use the tool iteratively as you negotiate rate, adjust down payment, or compare 15-year vs 20-year tenure with the same principal.

When first-time buyers should model the loan

- Before property shortlisting. Know your comfortable EMI band so you do not tour homes outside your real budget.

- After pre-approval. Banks may approve more than you should borrow. Model the sanctioned amount and a lower principal.

- Rate type decisions. Compare fixed-rate scenarios here; discuss floating spreads separately with your lender.

- Tenure selection. See how five extra years change total interest on the same home price.

- Co-borrower planning. Export CSV amortization to align with a spouse on prepayment and surplus goals.

- Invest vs prepay. Balance EMI with SIP Calculator on remaining monthly income after housing costs.

If you are also comparing personal loans for furnishing or renovation, read how to calculate personal loan EMI before applying for a focused personal-loan workflow.

Step-by-step: model a first home loan

Open EMI Calculator. Subtract your planned down payment from property price to get loan principal—for example, ₹80 lakh property with ₹20 lakh down means ₹60 lakh principal.

- Enter loan amount. Set principal (e.g., 6000000) via slider or typed input.

- Set annual interest rate. Use the rate from your lender offer. Even 0.25% matters on large principals.

- Choose tenure in years. Common home loans run 15–20 years. Try two tenures and compare total interest.

- Review EMI vs total interest. Confirm monthly payment fits income and total interest is acceptable—not just the EMI.

- Read insight text. On large loans, interest often rivals or exceeds principal; let that inform tenure and prepayment plans.

- Optional: Enable Prepayment. Model annual bonus contributions per ${PREPAYMENT_GUIDE} to see realistic savings.

Download month-wise CSV when you need a record for joint decision-making or financial advisor review. Highlight the first five years of interest payments to show co-borrowers how slowly principal drops without prepayment—a visual argument for maintaining an emergency fund before aggressive extra payments.

Benefits for first-time home buyers

- Reality check before emotional buys. Numbers anchor decisions when property marketing pushes urgency.

- Tenure transparency. See the rupee cost of stretching EMI comfort over more years.

- Prepayment roadmap. Advanced Options show how future bonuses shorten the loan.

- Private iteration. Test sensitive income and loan figures without uploading data.

- Instant comparisons. Re-run scenarios as developers, banks, or brokers revise offers.

- Holistic planning. Pair results with SIP Calculator to avoid a home purchase that blocks all investing.

Privacy and security

Home loan modeling often involves large principals tied to personal finances. The EMI Calculator processes everything locally—no loan amounts or rates are sent to UseBoldTools servers.

Exported CSV files remain on your device. Store or delete them thoughtfully on shared family computers.

Results are estimates. Lenders may apply different rounding, insurance mandates, or fee structures than this tool displays.

Common home loan mistakes to avoid

- Borrowing the maximum sanctioned amount. Pre-approval is a ceiling, not a target. Model a lower principal in EMI Calculator.

- Ignoring total interest. A manageable EMI on a 20-year loan can still mean enormous cumulative interest—see ${EMI_VS_INTEREST}.

- Minimal down payment without a plan. Smaller down payments raise principal, EMI, and interest. Compare scenarios before you optimize only for upfront cash.

- Choosing tenure for EMI alone. Five extra years can cost far more than the monthly relief suggests.

- Skipping prepayment planning. Assuming you will prepay “someday” without modeling is how bonuses get spent elsewhere.

- Forgetting non-EMI costs. Maintenance, tax, insurance, and furnishing sit beside EMI—leave room in your budget.

- Neglecting emergency fund. Homeowners need liquidity beyond EMI; do not prepay or over-borrow into a cashless position.

- Ignoring rate type mix-ups. Fixed and floating products behave differently over time; model fixed scenarios here and discuss float spreads with your lender separately.

- Overlooking life-stage changes. Childcare, school fees, or career breaks can strain EMI later—leave buffer beyond today’s surplus.

Best practices for first-time buyers

- Model loan principal after down payment, not full property value.

- Compare at least two tenures and record EMI, total interest, and total payment for each.

- Negotiate interest rate before finalizing property—small rate wins compound over decades.

- Plan prepayment scenarios in Advanced Options when you expect predictable annual surpluses.

- Keep total housing costs—including EMI, insurance, and maintenance—within a conservative share of stable income.

- Run SIP Calculator on post-EMI investable surplus so home ownership does not pause all long-term wealth building.

- Revisit EMI Calculator after rate changes, salary shifts, or when considering balance transfer.

More calculators for borrowers and investors are listed in the financial tools category.

Conclusion

First-time home loans lock in decades of cash flow. Avoiding common mistakes starts with seeing EMI and total interest together—not just the monthly quote. UseBoldTools EMI Calculator gives you that view, plus prepayment and amortization detail, before you commit.

Open EMI Calculator with your target property numbers, then read EMI vs total interest explained, how prepayments reduce loan interest, and how to calculate personal loan EMI before applying for a complete borrowing toolkit. Balance housing with investing via SIP Calculator on the financial tools category.

Frequently asked questions

What is the biggest home loan mistake first-time buyers make?

Many buyers maximize loan amount and tenure to afford a larger EMI-friendly payment, then overlook total interest and long-term cash flow. Modeling EMI and total interest before sanction helps avoid over-leveraging.

How much down payment should I plan for?

Lenders often finance up to a percentage of property value, but a larger down payment reduces principal, EMI, and total interest. Use the EMI Calculator with different loan amounts to compare.

Should I choose the longest tenure to lower EMI?

Longer tenure reduces monthly EMI but usually increases total interest substantially on a 15- to 20-year home loan. Compare both figures before choosing comfort over cost.

Can the EMI Calculator model home loans?

Yes. Enter your home loan principal after down payment, annual interest rate, and tenure in years up to 30. Review total interest and use Advanced Options for prepayment planning.

How does home buying relate to SIP planning?

EMI commitments reduce monthly surplus available for investing. Model loan payments here and use the SIP Calculator on remaining investable income to balance property and wealth goals.

Related guides

How to Calculate Personal Loan EMI Before Applying

Calculate personal loan EMI before applying with UseBoldTools: set amount, rate, and tenure, see monthly EMI and total interest instantly, and compare scenarios in your browser.

EMI vs Total Interest: How to Understand Your Loan Cost

Understand EMI vs total interest with UseBoldTools: see monthly EMI, total interest, donut chart split, and amortization so you know the true cost of your loan.

How Prepayments Can Reduce Your Loan Interest

See how prepayments reduce loan interest with UseBoldTools: simulate lump sums and extra monthly payments, view interest saved, tenure reduced, and month-wise breakdown locally.

Related tools

Ready to try EMI Calculator?

Use our free EMI Calculator tool in your browser — no account required for most workflows.

Open EMI Calculator