Financial Tools

EMI vs Total Interest: How to Understand Your Loan Cost

Understand EMI vs total interest with UseBoldTools: see monthly EMI, total interest, donut chart split, and amortization so you know the true cost of your loan.

By UseBoldTools Team 7 min readPublished July 2, 2026

Introduction

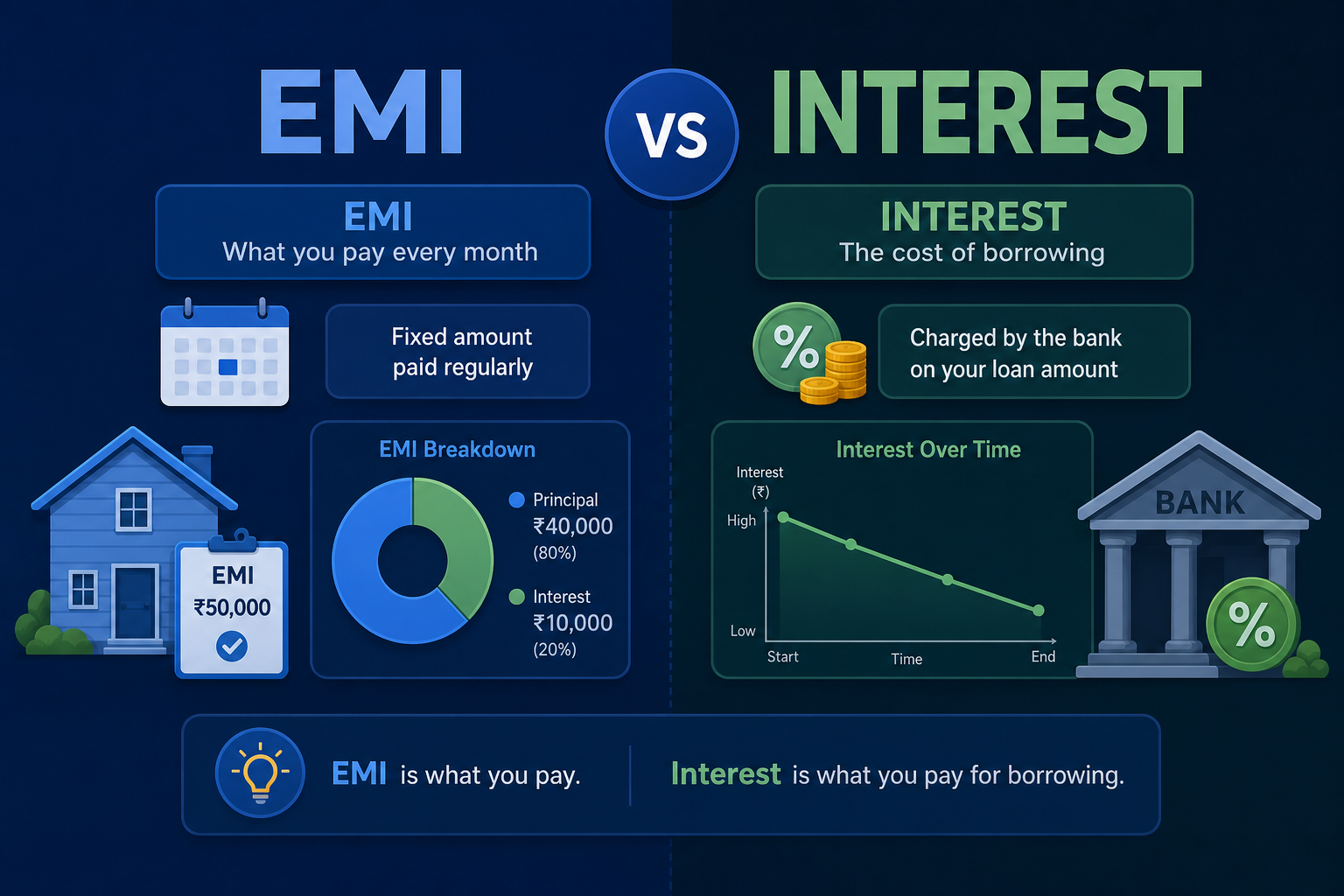

Loan marketing highlights one friendly number: the monthly EMI. That figure tells you whether the payment fits this month’s budget, but it does not, by itself, explain the full price of borrowing. Total interest—the money you pay beyond the principal—often surprises borrowers who never looked past the installment line. The free EMI Calculator on UseBoldTools shows EMI, total interest, and total repayment together so you can judge real loan cost.

This guide explains EMI vs total interest and how to understand your loan cost using the UseBoldTools results panel, donut chart, amortization table, and insight text. If you have not modeled your loan yet, start with how to calculate personal loan EMI before applying. For strategies to cut interest after you understand the baseline, read how prepayments reduce loan interest.

More financial planning guides live on the UseBoldTools blog.

Indian borrowers often anchor on EMI because it maps directly to monthly salary credits. That habit makes sense for cash-flow planning, but it hides the compounding effect of interest over 36, 60, or 84 monthly installments. A ₹15,000 EMI on a ₹5 lakh loan at 14% for five years carries a very different total interest than the same EMI stretched across seven years on a larger principal. Seeing both numbers prevents expensive surprises after disbursement.

How the calculator presents loan cost

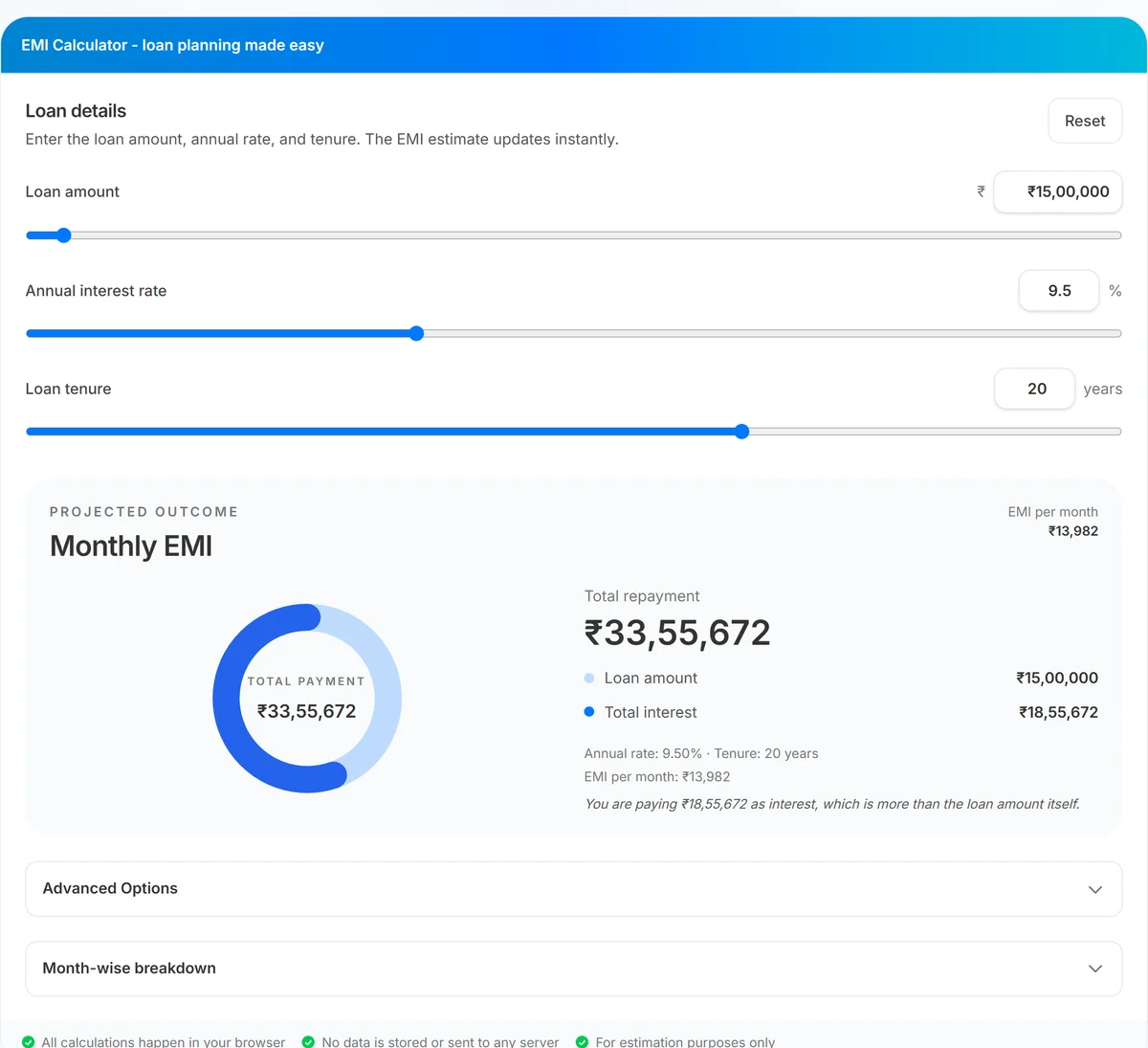

UseBoldTools EMI Calculator computes EMI with the standard fixed-rate formula, then derives total payment as EMI multiplied by the number of months in your tenure. Total interest is total payment minus loan amount. All three numbers update instantly when you change principal, annual rate, or years.

The Projected outcome card displays monthly EMI prominently, with total repayment as the large figure inside the donut chart. Blue segments split principal (lighter) and interest (darker) so you can see at a glance whether interest dominates. A summary line below states total interest in rupees and compares it to principal—for example, when interest exceeds half the loan amount.

Month-wise breakdown lists each installment’s principal portion, interest portion, optional extra payment, and remaining balance. That table proves why total interest grows: in early months, interest takes a larger share of each EMI even though the payment amount stays fixed.

Consider a ₹50 lakh home loan at 9% for 20 years. The EMI may look manageable relative to household income, but total interest can approach or exceed ₹57 lakh over the full term—more than the original principal in some cases. The calculator’s insight line exists precisely to surface that relationship without manual spreadsheet formulas. When the darker interest slice in the donut chart grows large, treat it as a signal to revisit tenure, down payment, or prepayment plans.

When total interest matters more than EMI

- Long-tenure home loans. A 20- or 25-year mortgage can cost more in interest than the property principal at typical rates.

- Rate shopping. Two lenders with similar EMI may differ by lakhs in total interest if rates diverge by even 0.25%.

- Tenure extension. Refinancing to a longer tenure cuts EMI but can restart heavy interest accrual on a large balance.

- Affordability vs optimality. You may afford the EMI while still overpaying interest relative to a shorter loan.

- Investment trade-offs. Money spent on interest is money not invested. Compare loan cost with expected returns from SIP Calculator on the same monthly surplus.

First-time home buyers often underestimate interest on 15- to 20-year loans. common home loan mistakes for first-time buyers covers tenure, down payment, and insurance pitfalls that inflate total cost beyond EMI.

Step-by-step: read EMI vs total interest

Open EMI Calculator and enter your loan amount, annual interest rate, and tenure in years.

- Note monthly EMI. This is your cash outflow each month. Use it for budget planning.

- Read total interest. Find the line labeled Total interest in the results panel. This is the cumulative interest over the full tenure at the entered rate.

- Compare to loan amount. Divide total interest by principal mentally—or read the insight line—to see if interest is a small add-on or a major second cost.

- Inspect the donut chart. The darker blue slice is interest. When it approaches half the circle, interest is a substantial share of everything you repay.

- Open Month-wise breakdown. Scroll early rows: interest columns are larger relative to principal. Later rows flip as the balance shrinks.

- Adjust tenure. Add five years and watch total interest rise even if EMI drops. That trade-off is the core EMI vs total interest lesson.

Export CSV from the breakdown section if you want to chart principal vs interest paid per year in a spreadsheet. Summing the interest column by calendar year helps you see how much you pay in years one through five versus years fifteen through twenty—a perspective that pure EMI quotes never provide.

Benefits of seeing both EMI and total interest

- Honest comparison. Compare lenders on total cost, not just the installment quote.

- Tenure clarity. See exactly how many extra lakhs a longer loan costs before you choose comfort over savings.

- Visual intuition. The donut chart makes abstract interest tangible without manual spreadsheet work.

- Amortization literacy. Month-wise rows teach how reducing balance changes each payment’s split.

- Prepayment motivation. Large total interest numbers make a stronger case for extra principal payments.

- Private modeling. Sensitive loan scenarios stay in your browser while you iterate.

Privacy and security

Interest and EMI calculations execute locally in your browser. UseBoldTools does not receive your loan inputs for processing or storage. That is important when modeling real mortgage or personal loan figures tied to your income.

CSV downloads are saved to your device only. Treat exported amortization schedules like any financial document on shared computers.

Displayed totals are estimates based on fixed rates and regular EMIs. Actual lender schedules may round differently or include fees not shown here.

Common mistakes when reading loan cost

- Treating EMI as the full price. Affordable monthly payments can still mean expensive total interest.

- Ignoring rate impact. Small rate differences compound over hundreds of installments.

- Choosing maximum tenure. Lowest EMI often means highest total interest on the same principal.

- Forgetting floating rates. This calculator models fixed rates. Floating loans can change total interest if rates rise.

- Skipping amortization review. The month-wise table reveals when you finally start paying meaningful principal.

- Comparing EMI across different principals. A lower EMI on a larger loan may still cost more in total interest.

After you understand baseline interest, simulate reductions with how prepayments reduce loan interest using Advanced Options in EMI Calculator.

Best practices for understanding loan cost

- Always record EMI, total interest, and total repayment when comparing two offers.

- Run the same principal with ±2 years tenure to see interest sensitivity before committing.

- Negotiate rate first; even a 0.25% reduction can save substantial interest on large home loans.

- Pair loan modeling with investment projections on SIP Calculator to decide prepay vs invest trade-offs.

- Use month-wise breakdown to plan when partial prepayment has the highest interest-saving impact.

- Revisit calculations after major life changes—salary jumps, bonuses, or rate resets.

Browse the financial tools category for SIP Calculator and other calculators that complement debt planning.

Conclusion

EMI tells you what leaves your account each month; total interest tells you what the loan truly costs. UseBoldTools EMI Calculator puts both numbers—and a visual split—on one screen so you can make informed borrowing decisions.

Open EMI Calculator to compare scenarios, then explore how prepayments reduce loan interest and how to calculate personal loan EMI before applying for application-ready and interest saving workflows.

Frequently asked questions

What is the difference between EMI and total interest?

EMI is your fixed monthly payment covering principal and interest. Total interest is the sum of all interest charges over the loan tenure. Total payment equals principal plus total interest.

Why is total interest often higher than borrowers expect?

Early installments pay more interest than principal because interest is calculated on the remaining balance. Longer tenures and higher rates amplify total interest even when EMI feels affordable.

How does the EMI Calculator show total interest?

The Projected outcome panel lists total interest beside loan amount and total repayment. The donut chart shows the interest share visually relative to principal.

Does a lower EMI always reduce total interest?

No. Lower EMI from a longer tenure usually increases total interest. Lower EMI from a lower rate or smaller principal generally reduces total interest.

Can I reduce total interest without changing EMI?

Prepaying principal reduces future interest even if your scheduled EMI stays the same. Use Advanced Options in the calculator to simulate prepayment savings.

Related guides

How to Calculate Personal Loan EMI Before Applying

Calculate personal loan EMI before applying with UseBoldTools: set amount, rate, and tenure, see monthly EMI and total interest instantly, and compare scenarios in your browser.

How Prepayments Can Reduce Your Loan Interest

See how prepayments reduce loan interest with UseBoldTools: simulate lump sums and extra monthly payments, view interest saved, tenure reduced, and month-wise breakdown locally.

Common Home Loan Mistakes First-Time Buyers Make

Avoid common home loan mistakes as a first-time buyer: model EMI and total interest with UseBoldTools, compare tenure, plan prepayments, and balance investing with SIP.

Related tools

Ready to try EMI Calculator?

Use our free EMI Calculator tool in your browser — no account required for most workflows.

Open EMI Calculator